Relief Veterinarian Salary in Canada: What Locum Vets Are Actually Earning (2026)

Ask ten vets what a relief shift pays and you’ll get ten different answers — somewhere between “barely worth the drive” and “I made more last weekend than I did all of last week as an associate.”

So who’s right?

Technically, both. Which is exactly the problem.

If you’ve been trying to figure out whether relief work actually pays better than your associate role, or whether the people raving about it on Reddit are outliers, this guide is for you.

This guide unpacks the real numbers for relief vets: day and hourly rates by province, the shift types that pay best, and how the math really compares to a T4 position once CPP, taxes, and missing benefits enter the picture.

Maybe you’re looking for autonomy over your calendar. Maybe a more sustainable income. Maybe a complete career pivot. Either way, you should have the full financial picture before you decide.

Canadian Relief Vet Pay, by the Numbers

Let’s start where it matters: what do Canadian relief vets actually charge?

The quick answer? Most general practice relief vets bill $600 to $1,200 CAD per day, with experienced vets, ER coverage, and last-minute bookings stretching higher. Provincial demand, urban vs. rural, and the type of shift all move the needle.

But averages are slippery. Here’s a closer look.

National Snapshot for Canadian Relief Vets

Numbers below are pulled from Canadian job boards, salary surveys, and the locum community itself:

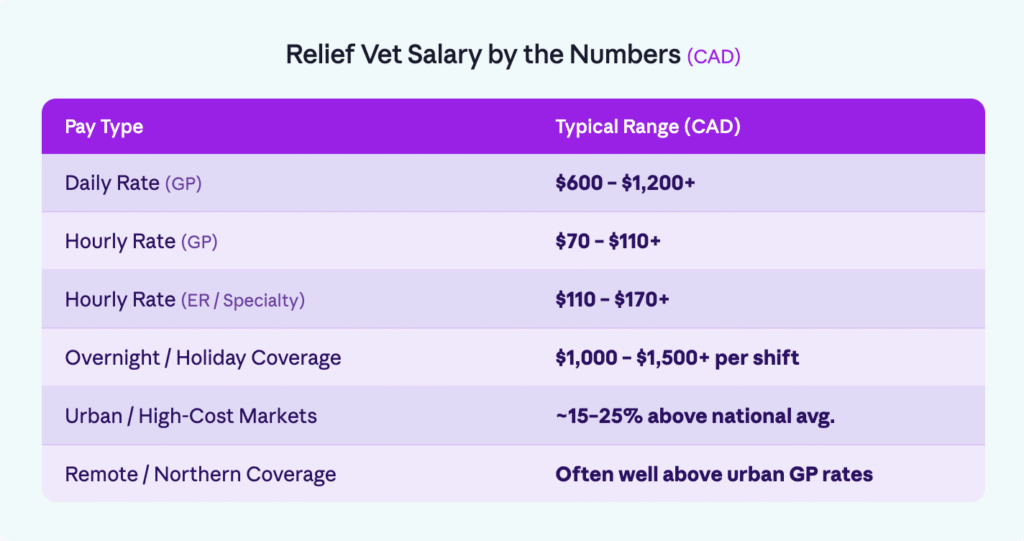

| Pay Type | Typical Range (CAD) | Notes |

| Daily Rate (GP) | $600 – $1,200+ | The standard structure for general practice shifts. Length, province, and how badly the clinic needs you all factor in. Rural and same-week bookings push the high end. |

| Hourly Rate (GP) | $70 – $110+ | More common for partial days or variable shifts. Most relief vets set a 6-hour minimum so a half-day booking doesn’t cost them a full day elsewhere. |

| Hourly Rate (ER / Specialty) | $110 – $170+ | Higher acuity, harder hours, fewer vets willing to do it. Toronto, Vancouver, and Calgary ERs sit at the top. |

| Overnight / Holiday Coverage | $1,000 – $1,500+ per shift | Premium territory — especially for stat holidays and short-notice fills. Some metro overnight ER shifts clear $1,500. |

| Urban / High-Cost Markets | ~15–25% above national avg. | Vancouver, Toronto, Calgary, and Ottawa. Reflects cost of living and tighter competition for available vets. |

| Remote / Northern Coverage | Often well above urban GP rates | Travel coverage, food animal work, and northern communities frequently bundle a premium rate with travel and accommodation. |

Sources: Glassdoor Canada, Indeed Canada, ZipRecruiter Canada, Government of Canada Job Bank, plus community insights from Canadian relief vet groups and r/Veterinary.

🧠 Pro tip: Most seasoned Canadian relief vets price by the day with a 6-hour minimum, then add a 1.5× overtime rate if the shift overruns. It keeps invoicing clean and it stops you from eating the cost when a clinic books you for “just a couple of hours” on a Saturday.

Relief Vet Pay by Province

Your postal code matters. Provinces with strong urban demand and higher costs of living consistently anchor the top of the pay range. The Atlantic provinces and small rural markets sit lower on paper, though chronic shortages are quickly closing that gap.

Here’s how relief pay shakes out across the country:

| Rank | Province / Region | Avg. Annual (CAD) | Avg. Hourly Rate | Quick Take |

| 1 | Alberta | $165,000 – $185,000 | $85 – $105 | Calgary and Edmonton anchor the top. Mixed-animal and rural shifts come with real premiums. |

| 2 | British Columbia | $160,000 – $185,000 | $85 – $100 | The Lower Mainland drives the average. Vancouver Island and the Interior are shortage zones. |

| 3 | Ontario | $150,000 – $180,000 | $80 – $100 | GTA and Ottawa run hot. Specialty and ER work routinely clears $100/hr. |

| 4 | Saskatchewan | $145,000 – $170,000 | $75 – $95 | High demand against a small talent pool. Mixed-animal practice pays especially well. |

| 5 | Quebec | $130,000 – $160,000 | $70 – $90 | Solid gross rates, but Quebec’s higher provincial tax brings net pay closer to the middle of the pack. |

| 6 | Manitoba | $130,000 – $155,000 | $70 – $90 | Winnipeg sets the floor; rural shifts often pay above the urban average due to shortages. |

| 7 | Nova Scotia | $115,000 – $145,000 | $65 – $80 | Halifax pulls the average up. Demand is rising faster than the supply of available DVMs. |

| 8 | New Brunswick | $110,000 – $140,000 | $60 – $80 | A smaller relief market, but shortages give you real negotiating room. |

| 9 | Newfoundland and Labrador | $110,000 – $140,000 | $60 – $80 | Limited relief market. Vets willing to travel are in high demand. |

| 10 | PEI | $115,000 – $145,000 | $65 – $80 | Small market but steady demand around Charlottetown and rural mixed practice. |

💡 Pro tip: Provincial averages mask a lot of the upside. Even in lower-paying regions, urban centres, ER coverage, and last-minute shifts routinely pay above the headline number. Northern and remote bookings usually come bundled with travel, accommodation, or a meaningful daily premium.

Sources: Aggregated from Glassdoor Canada, Indeed Canada, ZipRecruiter Canada, Job Bank, and Talent.com, current to early 2026. We’ve used ranges instead of single numbers because different sources report different medians depending on their methodology.

T4 vs. Self-Employed: The Comparison Most Vets Get Wrong

Most relief vets in Canada operate either as self-employed sole proprietors or through their own CCPC (Canadian-Controlled Private Corporation). That single structural shift changes nearly every line on your financial picture.

| Category | T4 Associate Vet | Self-Employed Relief Vet |

| Base Compensation | $95K–$135K/year | Variable. Gross hourly and day rates usually run higher |

| Extended Health & Dental | ✅ Frequently included | ❌ On you (or routed through your corp) |

| RRSP Match / Retirement | ✅ Sometimes offered | ❌ Self-directed |

| CPP Contributions | Split with employer | ❌ Both halves on you (11.9% combined in 2026 on income $3,500–$71,300) |

| EI | ✅ Deducted automatically | ❌ Not available unless you opt in for special benefits |

| CE + Licensing Fees | ✅ Often reimbursed | ❌ Self-funded, but fully deductible |

| GST/HST | N/A | ✅ Register and collect once you cross $30K in revenue |

| Tax Withheld at Source | ✅ Employer handles it | ❌ You manage quarterly instalments |

| Write-offs / Deductions | ❌ Very limited | ✅ Real (CE, mileage, home office, insurance, supplies) |

| Autonomy & Flexibility | ❌ Bounded | ✅ Extensive |

In Canada, relief vets are business owners, not freelancers. The upside is genuine: higher gross income, more control, and meaningful tax planning room. The trade-off is that you’re now responsible for your own health coverage, both halves of CPP, your licensing and CE, your insurance, and four quarterly instalments to the CRA. With a decent accountant in your corner, those trade-offs tilt strongly in your favour.

🧮 Quick math (Ontario sole proprietor): Four 10-hour shifts a week at $850/day works out to $163,200 in gross billings. From that, expect roughly $8,000+ in CPP (paying both halves), HST collected and remitted on top of your invoices (clinics pay it, you pass it to CRA), and around 30–35% set aside for combined federal and provincial income tax once deductions are applied. Most full-time relief vets at this volume land in the $95K–$115K net range, and well above that once they incorporate and start retaining earnings inside the corp.

🧮 Quick math: Four 10-hour shifts a week at $900/day = $187,200/year before taxes and expenses. As a 1099, you’ll owe self-employment taxes and cover your own benefits — so take-home will be lower, though many relief vets still match or beat associate pay while working fewer days.

Find Relief Shifts on Your Terms

Enjoy flexibility, better pay, and total control over your schedule with Serenity Vet.

Does Relief Actually Pay Better?

Spend some time in any Canadian vet Facebook group and you’ll see relief work described as both “the best decision I ever made” and “more headache than it’s worth.”

Here’s what most articles skip: Relief isn’t automatically more lucrative, but it absolutely can be, with the right approach.

Let’s run the comparison with Canadian numbers.

📉 The Associate Picture (T4)

Say you’re a full-time associate in Ontario pulling in:

- $120,000/year base salary

- Plus:

- $4,500 in extended health + dental

- $2,500 toward CE and licensing

- $3,500 RRSP match

- 3 weeks paid vacation

- Professional liability covered by the practice

Total compensation: ~$134,000/year.

It’s stable, it’s predictable, and, if you’ve got a good team, it comes with mentorship and a sense of belonging. But your calendar belongs to the clinic, not to you.

💼 The Relief Picture (Self-Employed)

Now picture yourself running four shifts a week at around $850/day:

- $850 × 4 days × 48 weeks = $163,200 gross

From there, subtract:

- ~$8,000–$10,000 for CPP (both halves) and the benefits you’re now buying for yourself

- ~$3,000–$6,000 for CE, CVO/CVMA/provincial licensing, professional liability insurance, mileage, supplies, and accounting fees

- 2–4 unpaid weeks off (already factored in)

- A few hours a month for invoicing, HST returns, and bookkeeping

After federal and provincial tax, you’re looking at a net somewhere in the $100K–$120K range as a sole proprietor in most provinces — and noticeably more if you incorporate, retain earnings in the corp, and draw a mix of salary and dividends.

The pattern, in plain terms:

- More money than most associate roles, often for fewer working days

- Real control over which clinics you say yes to

- No safety net unless you build one

- An actual business — bookkeeping, deadlines, and all

The Incorporation Decision

Here’s where the Canadian playbook diverges sharply from the American one, and where most of the tax leverage lives.

When you incorporate as a CCPC, your active business income up to $500K qualifies for the small business deduction, taxed at roughly 9% federally plus a small provincial rate. Combined, you’re looking at something in the 12–15% range depending on your province versus personal marginal rates of 43–53% on income over ~$120K. That gap is exactly why high-earning relief vets so often go the corporate route.

The caveat: incorporation only pays off if you can leave money inside the company. If you withdraw everything every year to live on, the deferral advantage mostly disappears, and you’re left with extra legal and accounting bills.

The Canadian accountants’ rule of thumb: once you’re consistently grossing $150K+ and don’t need every dollar personally, sit down with a CPA who works with vets and run the actual numbers for your situation.

What Tips the Balance?

Whether relief becomes lucrative or just exhausting usually comes down to three things:

- Booking consistency. Patchwork shifts mean an income rollercoaster. Anchor clinics and recurring bookings? Relief can pull ahead of associate pay quickly.

- Business literacy. Are you tracking deductions? Filing HST on schedule? Setting aside for instalments? If not, the leakage is real.

- What you actually want from your career.

- Relief: autonomy, variety, ceiling

- Associate: structure, benefits, team, mentorship

There’s no universally correct answer, just the one that fits the life you want.

The Low-Risk Way to Test It

Plenty of Canadian vets ease in before going all-in:

- Pick up one relief shift a week alongside your associate role

- Use relief income to bridge a mat leave, sabbatical, or reduced-hours stretch

- Lean on relief during a between-jobs transition or a cross-province move

You can build relief income gradually and see how it compares to what you have now.

Making Relief Work Pay

Done well, relief work delivers on both income and quality of life. Done lazily, it’s just freelancing with extra paperwork.

Here’s where most relief vets either build something real or quietly drift back to full-time.

1. Be Selective About Which Shifts You Take

A shift is not a shift. If you’re only saying yes to standard weekday GP hours at the local going rate, you’re leaving meaningful money on the table.

- Stack the premium shifts: ER, holidays, and overnights pay measurably more

- Say yes to short-notice gaps: clinics often pay 20–30% above their usual rate when they’re truly stuck

- Look beyond the metro: shortage zones in Saskatchewan, northern BC, the Atlantic, and rural Quebec consistently outpay urban GP

- Choose clinics that respect your time: strong RVT teams and efficient workflows = better ROI per hour

2. Push Your Rates Up Over Time

Once you’ve built a track record you’re worth more than the local median. Start at the going rate, then move it:

Think of your rate as something that should evolve, not something you set once and forget:

- Revisit your rate every 6–12 months, especially after a stretch of consistent bookings or strong referrals

- Anchor to the market, not your old rate: check what newer relief vets in your area are quoting and make sure you’re priced above them, not alongside them

- Charge more for harder work: specialty shifts (surgery, dentistry, ultrasound, exotics, ER) and same-week or holiday coverage should always carry a premium

- Raise rates with new clinics first: it’s easier to set a higher number with a fresh clinic than to renegotiate upward with one that’s known you for two years.

💡 Sell value, not time. A relief vet who keeps the workflow steady, the clients calm, and the support staff happy is worth a premium — and any good practice manager already knows it.

3. Build Repeat Relationships With Clinics

Reliable + communicative + drama-free is, hands down, the most underrated growth strategy in relief work.

- Become the default name for a few anchor clinics

- Lock in recurring shifts further out (huge for HST instalments and cash flow planning)

- Lean into referrals from practice managers and other relief vets

You’ll cut your admin time and stabilize your income at the same time.

4. Run It Like an Actual Business

Self-employment income comes with obligations the CRA takes seriously. Treat it accordingly.

- Register for GST/HST once you pass $30,000 in revenue across four consecutive quarters. You’ll charge HST on invoices (rate depends on province — 5% GST in Alberta, 13% HST in Ontario, 15% across most of Atlantic Canada), collect it, and remit it. Input Tax Credits on business expenses come back the other way.

- Hold back 25–35% of every payment for tax, depending on your bracket and province

- Get on a quarterly instalment schedule if your annual tax bill will top $3,000

- Track every business expense: mileage, supplies, CE, licensing, professional liability, home office, phone, accounting

- Run the incorporation math once you’re consistently above $150K gross, but only with proper CPA advice

- Find an accountant who knows veterinary relief work specifically. The cost pays for itself, repeatedly.

The expense most new Canadian relief vets forget? Professional liability insurance.

As a T4 associate, it was bundled invisibly into your role, usually via CVMA or a practice carrier. The moment you go independent, it’s on you. No clinic will let you walk through the door without proof of coverage.

The good news: it’s not expensive. Canadian veterinary professional liability typically runs $500–$1,200 CAD/year through providers like the Canadian Veterinary Medical Association or private brokers, depending on your scope and how many provinces you’re licensed in.

File it alongside health insurance, CE, CPP, and your quarterly instalments — not a roadblock, just a line item. And like nearly all your business expenses, it’s deductible. Build it into your rate from the start so it never feels like a surprise.

5. Stop Doing the Admin Yourself

The fastest way to bleed away your relief income? Spending evenings managing email threads, contracts, scheduling, and chasing invoices across six clinics.

That’s exactly the problem Serenity Vet was built to solve — so the time you save goes into the shifts that actually pay. The flexibility is the whole point. Don’t lose it to admin.

Serenity Vet: Steady Income Without the Operational Drag

If you’ve read this far, one thing’s clear:

Relief work can be profitable — but the logistics can kill the momentum.

You didn’t go to vet school to chase invoices, negotiate rates, or juggle a dozen email threads just to get one shift booked. That’s where Serenity Vet comes in.

We built SerenityVet for relief vets who want:

- Transparent, premium pay

- Fast, reliable payouts

- Smart scheduling tools that prevent burnout

- Access to quality practices that value your time.

Whether you’re testing the waters or going all-in on relief, Serenity Vet makes the process actually work — for your income, your lifestyle, and your sanity.

TL;DR: Should You Make the Move?

Canadian relief work isn’t a hack. It’s not passive income, and it’s not free money. But for the right vet, it’s one of the most flexible, high-ceiling paths in Canadian veterinary medicine.

The short version:

Relief Probably Fits If You:

- Want real control over your schedule and which clinics you work in

- Enjoy variety and adapt quickly to new practice environments

- Are willing to run the business side — or use a platform like Serenity Vet to offload it

- Prioritize income ceiling and flexibility over employer-provided stability

Relief Probably Isn’t For You If You:

- Lean heavily on employer benefits and a group RRSP match

- Prefer one clinic, one team, one long-term relationship

- Don’t want to think about HST returns or quarterly instalments

- Are early in your career and need active mentorship.