Tax Guide for Relief Veterinarians in Canada

This article is for informational purposes only and does not constitute tax or legal advice. Tax laws change! Always consult a licensed CPA or tax professional for guidance specific to your situation.

Why Relief Vet Taxes Are Different in Canada

If you’ve moved from a salaried clinic position to relief work, or you’re just starting out as a relief vet, the shift in how your taxes work can come as a real surprise. As an employee, your clinic handled income tax withholding, paid half your Canada Pension Plan (CPP) contributions, and managed the administrative side of payroll. As a self-employed relief vet, all of that is now on you.

Most relief veterinarians in Canada work as independent contractors. The Canada Revenue Agency (CRA) treats your relief income as self-employment income, which means different forms, different deadlines, additional CPP obligations, and, once you hit a certain revenue threshold, GST/HST registration. There’s also a meaningful set of deductions available to you that employees can’t access.

This guide walks through everything you need to know: how the CRA sees your work, what you have to file, how to handle installment payments, and how to make the most of the deductions available to you.

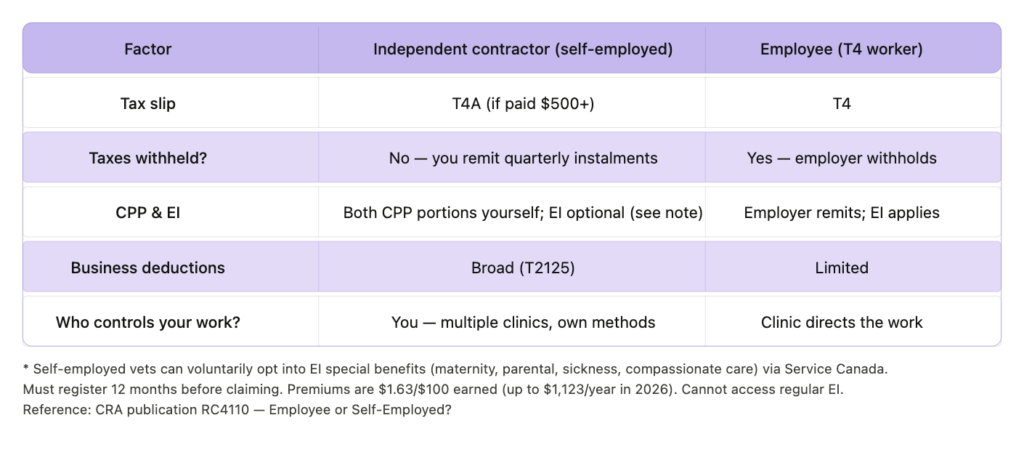

1. Employee or Self-Employed? How the CRA Decides

Before diving into deductions and deadlines, it’s worth understanding how the CRA classifies your working relationship because getting this wrong has real consequences for both you and the clinics you work with.

The CRA uses a multi-factor test to determine employment status. The key questions are:

- Does the clinic control how you do your work (not just what you do)?

- Do you provide your own tools and equipment?

- Can you profit or risk a loss from the arrangement?

- Can you work for other clinics at the same time?

Independent contractor (self-employed): You set your own schedule, work at multiple clinics, provide your own supplies where applicable, and invoice for your services. This is how most relief vets are classified. You’ll receive a T4A slip (rather than a T4) from any clinic that paid you $500 or more during the year.

Employee (T4 worker): Some clinics hire relief vets as employees, particularly for longer-term arrangements. If this is you, taxes are withheld from your pay and your employer handles CPP and EI remittances. Most of this guide is less relevant to you, though the deductions section may still apply if you have any self-employment income on the side.

Why it matters: Misclassification is a genuine risk in veterinary staffing. If a clinic is directing your work like an employee but paying you as a contractor, the CRA can reassess, forcing back-payment of CPP, EI, and penalties for both parties. If you’re ever unsure, the CRA’s publication RC4110 (Employee or Self-Employed?) is a useful reference.

2. Filing Basics: Your Key Forms and Deadlines

Your main forms

As a self-employed relief vet, you’ll file a T1 General (your personal income tax return) and attach Form T2125 — Statement of Business or Professional Activities. This is where you report your gross relief income and all your deductible business expenses. The net income from T2125 flows to Line 13500 of your T1, where it gets added to any other income you have for the year.

If you’ve registered for GST/HST (more on this below), you’ll also file a separate GST/HST return — usually annually, quarterly, or monthly depending on your revenue level.

Filing deadline: June 15, but payment due April 30

This is one of the most important things to know as a self-employed vet in Canada. The CRA gives self-employed individuals until June 15 to file their return, but any taxes you owe are still due on April 30. So you have extra time to file, but not extra time to pay. If you wait until June to calculate what you owe and then write a cheque, you’ll be paying interest on whatever was owing since April 30.

Practical tip: Have your return ready to file by late April regardless of the June deadline. That way you know exactly what you owe, can pay it by April 30, and avoid interest, then submit the actual return whenever you’re ready before June 15.

Federal income tax brackets

Canada uses a graduated federal income tax system. As of 2026, the federal brackets are: 15% on the first $57,375 of taxable income, 20.5% on the next portion up to approximately $114,750, 26% up to $158,519, 29% up to $220,000, and 33% on income above that. Provincial taxes are added on top, and rates vary significantly by province, so your combined marginal rate as a higher-earning relief vet can reach 50%+ in some provinces. This is part of what makes the deductions and incorporation discussions so meaningful.

3. CPP Contributions: You’re Paying Both Sides

As an employee, your employer pays half your Canada Pension Plan contributions and you pay the other half. As a self-employed person, you’re both the employer and the employee — so you pay the full amount.

For 2026, the self-employed CPP contribution rate is 11.9% of your net self-employment income, up to a maximum contribution of $8,460.90 for the year. This applies to income above a basic exemption of $3,500.

You calculate CPP contributions on Schedule 8 of your T1 return. The contributions are not optional, since they fund your eventual CPP retirement benefit.

The silver lining: you can deduct half of your CPP contributions as a non-refundable tax credit, and the other half as a business expense deduction. This reduces the after-tax cost somewhat, but it’s still a meaningful cash outflow to budget for.

Budgeting note: Factor CPP into how much you set aside from each payment. Combined with federal and provincial income taxes, most self-employed relief vets in Canada should be setting aside 28–35% of their gross income, depending on their province and income level.

Work with Great Clinics? Bring Them to Serenity Vet

Invite the clinics you already work with to Serenity. Scheduling, invoicing, and payments handled automatically, with no marketplace fees cutting into your rate.

4. Installment Payments: How the CRA’s Payment System Works

Because no one is withholding taxes from your relief payments throughout the year, the CRA may require you to pay your taxes in quarterly installments rather than one annual payment.

The threshold is straightforward: if your net tax owing exceeds $3,000 in net tax in the current year AND in either of the two previous years, you’ll need to make installment payments. (In Quebec, the threshold is $1,800 since Quebec administers its own provincial tax separately.)

The four installment due dates:

• March 15

• June 15

• September 15

• December 15

The CRA will typically send installment reminders in February and August with suggested amounts, either based on your prior year’s taxes or an estimate of your current year liability. You don’t have to use the CRA’s suggested amounts; you can calculate your own if your income has changed significantly.

You can make installment payments through your CRA Account, through online banking (the CRA is set up as a payee at most Canadian banks), or by cheque.

Missing installments doesn’t result in automatic penalties, but the CRA will charge interest on late or underpaid installments, and that interest is not deductible. It’s much easier to pay on time.

5. Deductions You Shouldn’t Miss

One of the genuine advantages of self-employment is access to business deductions. Everything you legitimately spend to earn your relief income can reduce your taxable income, and at Canadian marginal tax rates, those deductions add up quickly.

Vehicle expenses

Driving between clinics is core to relief vet work, and vehicle expenses are among the most valuable deductions available. You can deduct the business-use portion of your actual vehicle costs: fuel, insurance, maintenance, lease payments or depreciation (claimed as Capital Cost Allowance), licence fees, and loan interest. Keep a mileage log that records the date, destination, and purpose of each trip; the CRA expects you to track both business and personal kilometres so you can calculate the business percentage.

Home office

In practice, this is a harder deduction for relief vets to justify than it sounds, since the CRA’s “exclusively for business” requirement is strict. If you think you qualify, calculate the percentage of your home’s total square footage the workspace occupies and apply that to your eligible expenses, and it’s worth running it by your accountant before claiming it. Note that the pandemic-era flat rate ($2/day) method has been discontinued; the detailed method is required for 2026 and beyond.

Continuing education and professional development

Conference fees, online courses, webinars, and related travel expenses (flights, hotels, 50% of meals) for CE events are fully deductible. This is one of the more generously treated categories under CRA rules for professional practitioners.

Professional fees and licensing

Your provincial veterinary college membership fees, federal and provincial licensing fees, DEA or controlled substance permits, and professional liability insurance premiums are all deductible. Professional membership dues (CVMA and provincial associations) also qualify.

Equipment and supplies

Smaller equipment purchases (stethoscopes, scrubs, medical bags, office supplies) are generally deductible in the year you buy them. Higher-value items like a laptop or tablet used for work are treated differently: you claim them through Capital Cost Allowance (CCA), which allows you to deduct a portion of the cost each year rather than all at once. Your accountant can help you categorize these correctly.

Phone and internet

The business-use portion of your cell phone and home internet bills are deductible. Track what percentage of your usage is work-related and apply that to your bills — a reasonable, documented estimate is what the CRA expects.

Meals and entertainment

If you have a meal with a client or colleague for a legitimate business purpose, 50% of the cost is deductible. Keep a record of who you met with and what was discussed — the CRA may ask.

RRSP contributions

RRSP contributions reduce your taxable income, making them one of the most powerful year-end planning tools available to self-employed Canadians. You can contribute up to 18% of your prior year’s earned income, subject to an annual maximum ($32,490 for 2025). The RRSP contribution deadline for the 2025 tax year is March 1, 2026. Unused room from prior years carries forward indefinitely.

6. GST/HST: The One That Catches New Relief Vets Off Guard

The $30,000 threshold

Once your total taxable revenue from self-employment exceeds $30,000 in any four consecutive calendar quarters, you are required to register for a GST/HST account with the CRA. This is not optional: you have 29 days from the date you cross the threshold to register.

For most active relief vets working regularly, crossing $30,000 is a question of when, not if. If you’re earning even $800/week in relief fees, you’ll hit that threshold within the year.

What registration means in practice

Once registered, you need to charge GST or HST on your invoices to clinics, collect it, and remit it to the CRA periodically. The rate depends on the province where the service is provided: GST-only provinces charge 5% (Alberta, BC, Saskatchewan, Manitoba), while HST provinces charge between 13–15% (Ontario is 13%; New Brunswick, Newfoundland and Labrador, and Nova Scotia are 15%; PEI is 15%). Quebec operates its own QST system alongside the federal GST.

If you work across multiple provinces, you’ll apply the rate applicable to where the service is delivered, not where you’re based.

Input Tax Credits (ITCs) — the upside of registration

Here’s the good news about GST/HST registration: you can claim Input Tax Credits for the GST/HST you’ve paid on business purchases. Equipment, phone, software, vehicle fuel, CE courses — if you paid sales tax on it for your business, you can get it back. For many relief vets, the ITCs roughly offset much of the GST/HST administration burden.

Voluntary early registration

You can register for GST/HST voluntarily even before you hit $30,000. This makes sense if you’re spending significantly on equipment or other taxable purchases early on and want to start claiming ITCs right away.

Note for Quebec-based vets: Quebec administers its own provincial tax (QST) separately from the CRA. If you’re based in or working in Quebec, you’ll need to register with Revenu Québec for QST in addition to (or instead of, for the provincial component) the federal GST. The rules are similar but handled through a different agency.

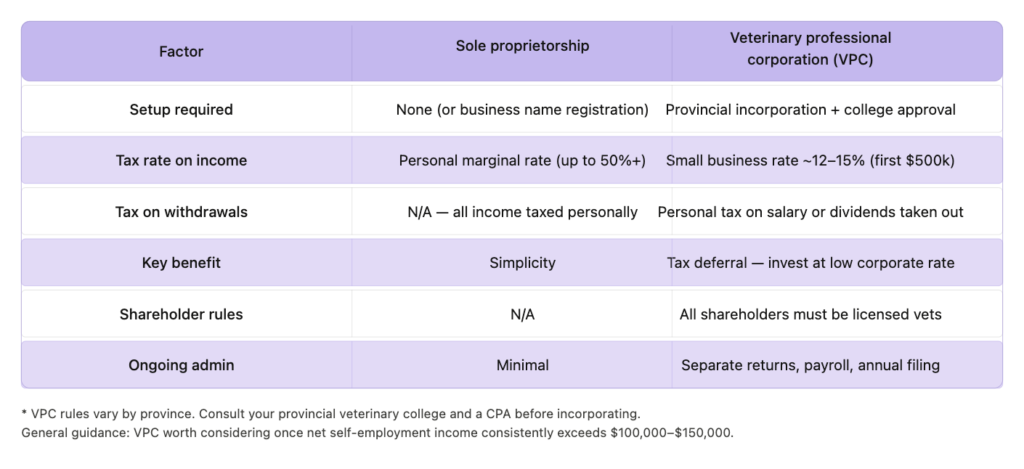

7. Business Structure: Sole Proprietor vs. Professional Corporation

Most relief vets in Canada start as sole proprietors and stay there until their income grows to a point where a different structure makes sense. Here’s an honest look at the options:

Sole Proprietorship

The simplest structure. No formal registration required (beyond potentially registering a business name). All income is yours and all tax is paid at your personal marginal rate — which, in high-income provinces, can reach 50%+. For vets earlier in their relief career or earning moderate income, the simplicity outweighs the tax cost.

Veterinary Professional Corporation (VPC)

This is the incorporation option specific to veterinarians in Canada. Each province has its own rules, but generally a licensed veterinarian can incorporate a professional corporation to practice veterinary medicine through.

The key tax advantage: corporate income up to $500,000 is taxed at the small business rate: approximately 9% federally plus a provincial rate, resulting in a combined rate of roughly 12–15% depending on your province. Compare that to a personal marginal rate of 45–53%. The difference can be very significant for high-earning relief vets.

The catch: you still pay personal tax when you take money out of the corporation as a salary or dividend. The benefit comes from tax deferral — you leave income in the corporation, invest it at the lower corporate rate, and draw it out in retirement when your personal marginal rate is lower.

Important restrictions: unlike regular corporations, all shareholders of a VPC must be licensed veterinarians. Family members who aren’t licensed vets generally cannot hold shares (unlike some other professional corporations). Rules vary by province: Ontario is governed by the College of Veterinarians of Ontario, for example.General guidance: If your net self-employment income is consistently above $100,000–$150,000, a conversation with a CPA about VPC incorporation is likely worth your time. The tax deferral benefits are real and substantial at that income level. But the administrative requirements( separate tax returns, payroll, annual filing) add meaningful complexity. Don’t incorporate before you need to.

8. Record-Keeping: What the CRA Expects

The CRA requires you to keep records that support everything you claim on your return, and to keep them for at least six years from the end of the tax year they relate to. For self-employed individuals, that means:

• All income received, with dates and amounts (T4A slips you receive should match your own records)

• Receipts for every business expense you claim

• A vehicle mileage log with date, destination, purpose, and kilometres for each business trip

• Home office records: floor plans or measurements, and receipts for utilities, internet, and rent/mortgage interest

• GST/HST records if you’re registered: invoices you issued showing the tax charged, and receipts for business purchases showing the tax you paid

Digital records are fine: the CRA accepts scanned copies of receipts and electronic records. Apps like Wave, QuickBooks Self-Employed, or even a well-organized folder of scanned receipts and a mileage tracking app work perfectly well.

The most important habit: reconcile your records monthly, not annually. Trying to reconstruct a year’s worth of invoices and receipts in March is stressful and error-prone.

9. When to Hire an Accountant

Many relief vets file their own taxes successfully for years, especially using CRA-certified software like TurboTax, Wealthsimple Tax, or UFile. But there are clear points where professional help pays for itself:

• Your first year of self-employment — getting T2125 right and understanding CPP and installment obligations is worth a one-time consult

• You’re crossing the $30,000 GST/HST threshold and need to set up your account and invoicing correctly

• You’re working across multiple provinces and have multi-province filing questions

• Your income has grown to where you want to discuss VPC incorporation

• You want a year-round tax planning strategy (RRSP timing, CCA claims, income deferral) rather than just year-end filing

Look for a CPA with experience in self-employed healthcare professionals or veterinarians specifically. Provincial CPA associations (CPA Ontario, CPA BC, etc.) have member directories. A CPA familiar with the veterinary sector will know the deductions, understand the GST/HST nuances, and be able to speak to incorporation options when the time comes.

The Bottom Line

Relief work in Canada comes with real tax complexity — more than most new independent contractors expect. The combination of self-employment income tax, full CPP contributions, GST/HST registration requirements, and provincial tax considerations means there’s more to manage than your average T4 employee faces.

But the tools to manage it well are straightforward: set aside 30–35% of every payment, keep tidy records year-round, make installment payments on time, register for GST/HST when you need to, and work with a CPA once your income justifies it. Do those things, and what looks complicated on the surface becomes a manageable (and often rewarding!) part of working independently.

Relief Work on Your Terms

Set your rates, choose your shifts, and get paid automatically — no chasing invoices, no middlemen.