Tax Guide for Relief Veterinarians (U.S.)

This article is for informational purposes only and does not constitute tax or legal advice. Tax laws change! Always consult a licensed CPA or tax professional for guidance specific to your situation.

1. Are You an Employee or an Independent Contractor?

Before anything else, it’s worth understanding how you’re classified because it shapes everything else in this guide.

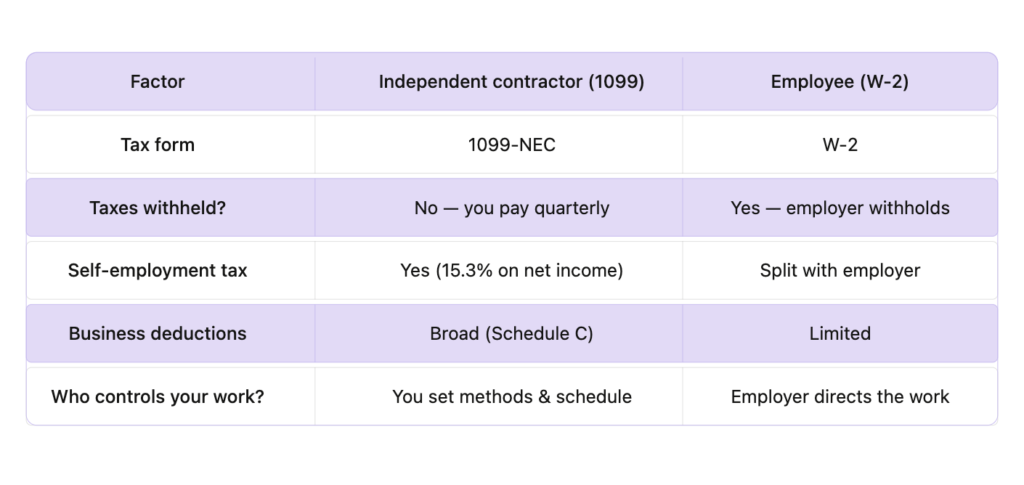

Independent Contractor (1099): This is the most common classification for relief vets. The clinic pays you a flat rate for your time, you invoice them (or they pay through a platform), and at tax time you receive a 1099-NEC form if you earned $600 or more from that client. You are responsible for all your own taxes.

Employee (W-2): Some clinics hire relief vets as actual employees. In this case, taxes are withheld from your paycheck and you receive a W-2. This guide is less relevant if this is your situation, though the deductions section may still apply if you have any 1099 income on the side.

Why it matters: Misclassification is a real issue in veterinary staffing. If a clinic is treating you like an employee — setting your hours, requiring you to use their equipment exclusively, directing how you work — but paying you as a contractor, that’s a potential legal and tax problem for both parties. The IRS has a behavioral and financial control test for this. If you’re ever unsure about your status, it’s worth a conversation with a CPA.

2. Filing Basics: What You’re Actually Required to Do

Your main form: Schedule C

As a self-employed relief vet, you’ll report your business income and expenses on Schedule C (Profit or Loss from Business), which gets filed alongside your personal Form 1040. Your net profit (income minus deductible expenses) is what you’ll actually pay taxes on.

Self-employment tax: 15.3%

Here’s the one that can catch new relief vets off guard. As an employee, you’d pay 7.65% in FICA taxes (Social Security + Medicare), and your employer pays the other half. As a self-employed person, you pay both sides — the full 15.3%. This applies to the first $176,100 of net self-employment income in 2026 for Social Security (12.4%), with Medicare (2.9%) continuing beyond that threshold. If your net income exceeds $200,000 as a single filer, an additional 0.9% Medicare surtax applies.

The silver lining: you can deduct half of your self-employment tax as an above-the-line deduction on your Form 1040, which slightly reduces your taxable income.

Federal income tax

On top of self-employment tax, you’ll owe federal income tax based on your tax bracket. Relief vets earning good incomes often land in the 22%–32% marginal brackets. A useful rule of thumb: set aside 25–30% of every payment you receive to cover both income tax and self-employment tax. Some vets in higher brackets set aside 35%.

State income tax

Most states also have income tax, and if you work across multiple states, you may need to file a return in each state where you earned income. A handful of states — including Texas, Florida, Nevada, and Washington — have no state income tax, which is a meaningful benefit if you’re based there.

Annual filing deadline

Your federal tax return is due April 15. You can request a six-month extension (to October 15), but keep in mind an extension to file is not an extension to pay — any taxes owed are still due in April.

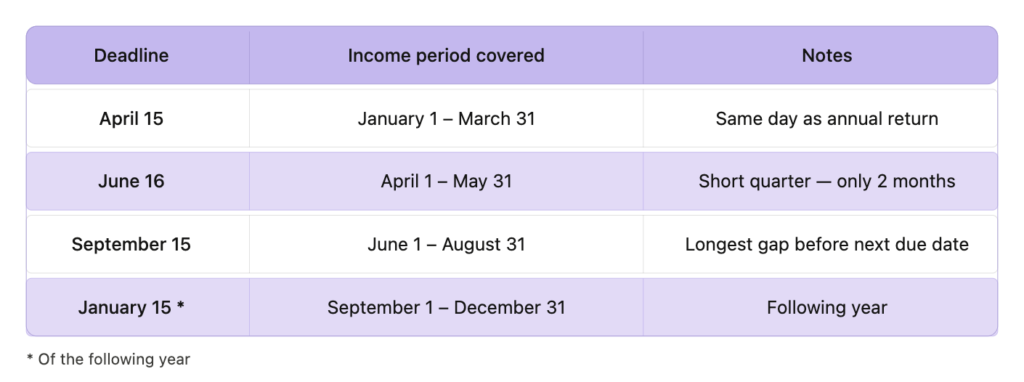

3. Quarterly Estimated Payments: Don’t Skip These

Because no one is withholding taxes from your relief vet payments, the IRS expects you to pay as you go throughout the year. These are called estimated tax payments, and missing them can result in underpayment penalties — even if you pay your full tax bill in April.

The four quarterly deadlines:

• April 15 — covers January 1 to March 31

• June 16 — covers April 1 to May 31

• September 15 — covers June 1 to August 31

• January 15 (of the following year) — covers September 1 to December 31

You can make payments through the IRS’s free EFTPS system or directly at IRS.gov.

How much to pay:

You can avoid penalties by paying either 90% of what you’ll owe for the current year, or 100% of what you owed last year (110% if your prior-year AGI exceeded $150,000). Most new relief vets default to the prior-year safe harbor until they get a feel for their income patterns.

Practical tip: Open a separate savings account just for taxes. Every time you receive a relief payment, transfer 25–30% into that account immediately. It removes the temptation to spend it and means you’re never scrambling when a payment is due.

Work with Great Clinics? Bring Them to Serenity Vet

Invite the clinics you already work with to Serenity. Scheduling, invoicing, and payments handled automatically, with no marketplace fees cutting into your rate.

4. Deductions You Shouldn’t Miss

This is where being self-employed really pays off. As an independent contractor, you can deduct ordinary and necessary business expenses, meaning anything that’s common and appropriate for your work as a relief vet. Here are the main categories to know about:

Mileage and vehicle expenses

Driving between clinics is a core part of relief vet work, and every business mile is deductible. For 2026, the IRS standard mileage rate is 72.5 cents per mile. Keep a mileage log with dates, destinations, and business purpose: a mileage tracking app makes this painless. Note that your commute from home to a regular workplace is not deductible, but driving to different clinic locations generally is.

Continuing education

Conference fees, online courses, CE subscriptions, and related travel (when you travel more than 50 miles from home for a CE event, airfare, lodging, and 50% of meals are deductible) all qualify. This is one of the more generous deductions available to relief vets.

Licensing and professional fees

Your state veterinary license, DEA registration, professional liability insurance premiums, and memberships in organizations like AVMA or specialty associations are fully deductible.

Equipment and supplies

Stethoscopes, medical bags, scrubs, protective gear — if you bought it for your practice, it’s generally deductible.

Health insurance premiums

If you pay for your own health insurance (and you’re not eligible for coverage through a spouse’s employer plan), you can deduct 100% of those premiums as a business expense. This is a significant deduction that W-2 employees generally don’t have access to.

Retirement contributions

Contributing to a Solo 401(k) or SEP-IRA reduces your taxable income and builds your retirement savings simultaneously. For 2026, Solo 401(k) contributions can reach up to $70,000 total (employee + employer contributions), making this one of the most powerful tax-reduction tools available to self-employed vets.

Phone and internet

You can deduct the business-use percentage of your cell phone and home internet bills. Keep it reasonable: if you use your phone 60% for work, deduct 60%.

Qualified Business Income (QBI) deduction

Under current tax law, many self-employed veterinarians can deduct up to 20% of their qualified business income. However, because veterinary practice is classified as a health services business, this deduction phases out at higher income levels. Your CPA can tell you whether and how much you qualify for.

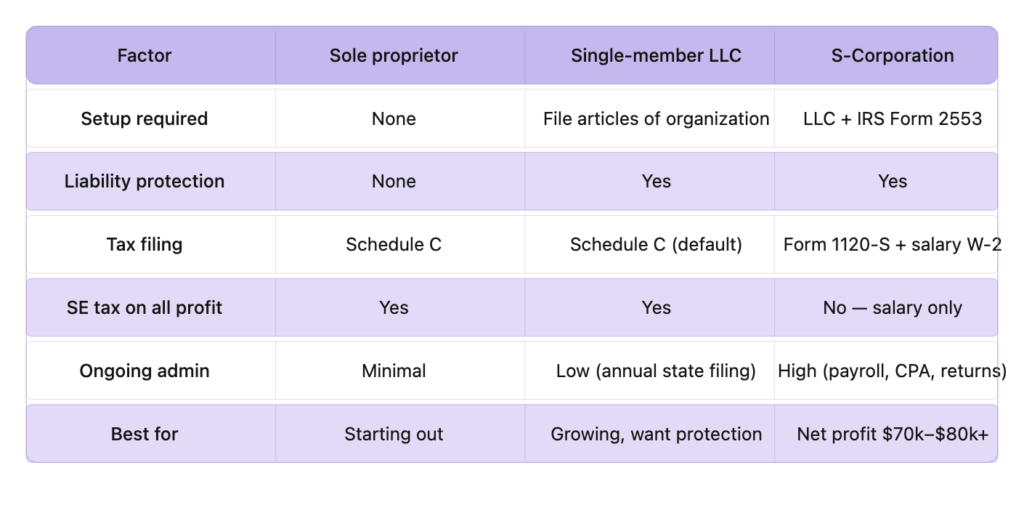

5. Business Structure: Sole Proprietor vs. LLC vs. S-Corp

Business Structure: Sole Proprietor vs. LLC vs. S-Corp

Most relief vets start out as sole proprietors: it requires no formal setup, and your Schedule C handles everything. As your income grows, though, it’s worth understanding your options.

Sole Proprietor The default. No setup required. All income and expenses flow through Schedule C. Simple, but provides no liability protection and offers no way to reduce self-employment taxes beyond deductions.

Single-Member LLC An LLC gives you personal liability protection — separating your personal assets from your business — but by default is taxed the same as a sole proprietorship. It’s a good middle ground for many relief vets, providing legal protection without extra tax complexity.

S-Corporation Election This is where things get interesting for higher-earning relief vets. When you elect S-Corp status, you pay yourself a reasonable salary (on which you pay self-employment taxes), and take additional profit as distributions (which are not subject to self-employment tax). On $50,000 in distributions, for example, that’s potentially $7,500 in SE tax savings — real money worth planning around.

The good news for relief vets is that this threshold is genuinely achievable. Strong day rates mean $80,000+ in net profit is a realistic outcome within a year or two of working steadily, and because relief work typically involves no employees or inventory, the administrative burden is more manageable than it would be for many other self-employed professionals.

That said, S-Corp status isn’t free to maintain. You’ll need to run payroll, file a separate business tax return (Form 1120-S), and pay yourself a “reasonable salary”, which the IRS takes seriously for licensed professionals. You can’t pay yourself $30,000 and take $100,000 in distributions; for a veterinarian, the reasonable compensation bar is fairly high given the professional skill involved. Factor in payroll software or service costs ($500–$2,000/year) and higher CPA fees before assuming the savings pencil out. State-level treatment also varies, and some states tax S-Corps in ways that erode the federal benefit.

General guidance: If you’re just starting out, a sole proprietorship or simple LLC is fine. Once your net relief income consistently exceeds $70,000–$80,000, a conversation with a CPA about S-Corp election is worth having.

6. Record-Keeping: What to Track and How

Good records are the foundation of stress-free tax filing and your best protection in the unlikely event of an audit. Here’s what you should be tracking year-round:

• All income received, by date and client (your 1099s should match your own records)

• Every business expense, with receipts (even photos of paper receipts stored in an app works)

• A mileage log for every business drive

• Invoices sent and payments received

• Home office square footage and related expenses if claiming that deduction

A few practical tools that relief vets commonly use: QuickBooks Self-Employed, Wave (free), FreshBooks, or even a well-organized spreadsheet. The key is consistency: updating records monthly is far easier than reconstructing a year’s worth of transactions in March.

One more thing: keep business and personal finances separate. Open a dedicated business checking account and run all clinic payments and business expenses through it. This makes record-keeping dramatically simpler.

7. When to Hire an Accountant

You can absolutely DIY your taxes as a relief vet, especially early on when your situation is straightforward. But there are some clear signs it’s time to bring in a professional:

• You’re earning significant 1099 income for the first time and aren’t sure what to set aside

• You work across multiple states and need to navigate different filing requirements

• You’re considering setting up an LLC or S-Corp

• You want to maximize retirement contributions and aren’t sure which plan is best

• Your income has grown to the point where tax planning (not just tax prep) could save you thousands

Look for a CPA who has experience with self-employed healthcare professionals or veterinarians specifically — they’ll be familiar with the common deductions and planning opportunities that apply to your situation. It’s money well spent.

The Bottom Line

Relief work gives you real flexibility and earning potential, but it comes with tax responsibilities that salaried employment doesn’t. The vets who handle it best are the ones who treat taxes as a year-round habit rather than an annual scramble: setting aside money consistently, tracking expenses as they happen, making quarterly payments on time, and working with a good CPA once the complexity warrants it.

Get those habits in place early, and tax season becomes a lot less daunting.

Relief Work on Your Terms

Set your rates, choose your shifts, and get paid automatically — no chasing invoices, no middlemen.